Despite the decline in stock prices, digital banks continue to grow.

Sofi Technologies (Sophie -3.59%) The share price decline has to be one of the biggest disappointments of the year, after shares more than doubled last year and the company entered 2024 on a strong note after posting its first-ever profit.

While the company continues to report solid growth and has posted three consecutive quarters of profits, SoFi shares are down more than 20% this year. The market is making a mistake, and you could profit from the stock’s decline before the market realizes it.

SoFi is revolutionizing traditional banking

SoFi is a comprehensive financial services platform that offers lending services, banking products, and more through a digital app. It has no physical branches and targets students and young professionals, a demographic that values digital, consumer-centric experiences. SoFi has attracted millions of members looking for better products, and these customers skew younger, positioning the company for long-term growth as the market matures and engagement with the SoFi platform increases.

The second quarter earnings report was full of positive news: membership grew 41% year over year to approximately 8.8 million, adjusted net revenue increased 20%, and generally accepted accounting principles (GAAP) net income was $18 million. Management raised its 2024 adjusted net revenue and earnings per share (EPS) outlook and now expects positive net income for the third quarter and full year.

SoFi is more than just a lender

At first glance, it’s unclear exactly what’s troubling the market, but concerns about slowing lending growth are likely contributing to the share price decline. But while SoFi is eager to show off its new vertical and how it’s hedging against lending pressures, it doesn’t appear to have taken over the credit business just yet.

SoFi has expanded into a wider range of services: Besides its core lending division, it now has two other divisions: its technology platform, or white-label financial infrastructure services under the Galileo brand, and financial services, which are non-lending services.

These two businesses are growing at a much faster pace than lending, and are attracting many users even in tough times when the lending business is under pressure. They increase revenue and relieve the pressure on lending, but what they are really achieving is building a broad base of services that members can increase their engagement with. We are already seeing positive results from this model, but it will become even more beneficial over time as more members join the platform.

But the lending division is still sizable. It accounted for 55% of second-quarter revenue, and while other divisions have boomed, the core division hasn’t seen much growth. Lending revenue in the second quarter was $341 million, up 3% from last year. The other two divisions grew 46% year over year in the second quarter, but are still fairly small.

Lending contribution margin was $198 million, up 8% year over year. Combined financial services and technology platform contribution margin was $86 million. This is where you really see the value of the lending platform to SoFi’s business. It is concerning that lending contribution only increased 8% even as technology platform contribution increased 82% and financial services went from loss to profit.

The company overall posted a profit, but that profit was mainly due to a slowdown in its lending business, and the market is sensing the trouble until other divisions take over a larger part of the business and contribute more to the consolidated results.

Wake up before the market

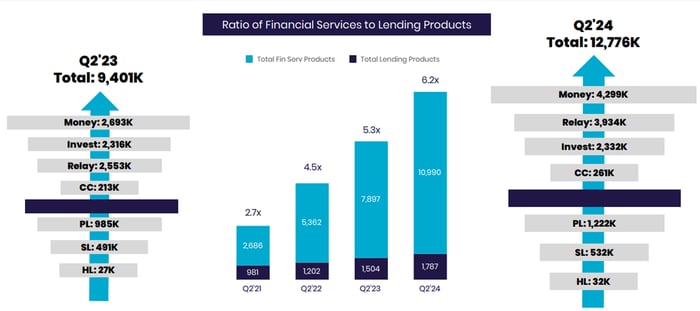

Fortunately for SoFi and its shareholders, the pessimism the market is pricing in seems unfounded when considering the long-term opportunity. Despite the results already being achieved, the market is not ready to be confident in the potential of SoFi’s new business. Here’s a visual representation of the growth of the non-lending segment:

Image credit: SoFi.

SoFi’s expansion plans are on track, and new members and increased engagement should eventually overcome the short-term weakness in the lending division. However, interest rates will likely be lowered first, which should allow SoFi’s lending division to recover. All of this combined makes it a very attractive long-term investment.

#market #hugely #wrong #SoFi #Heres #Motley #Fool